When you trade a bitcoin contract on Kalshi, the strike gets all your attention — "above $108,000," "up or down," "between $105K and $110K." But the strike is only half the question. The other half, the one most traders never check, is what price gets compared to that strike when the window closes. That's the settlement source, and on Kalshi's bitcoin markets it's both more standardized and more misunderstood than the guides suggest.

The short version: every Kalshi bitcoin contract, from the fifteen-minute up/down all the way out to the yearly, settles on a 60-second average of the CF Benchmarks Bitcoin Real-Time Index. Same mechanism, same index, every frequency. This is the full breakdown — the exact mechanism, why averaging beats a last-price snapshot, the persistent "BRRNY vs BRTI" myth, and the edge cases that actually cost traders money.

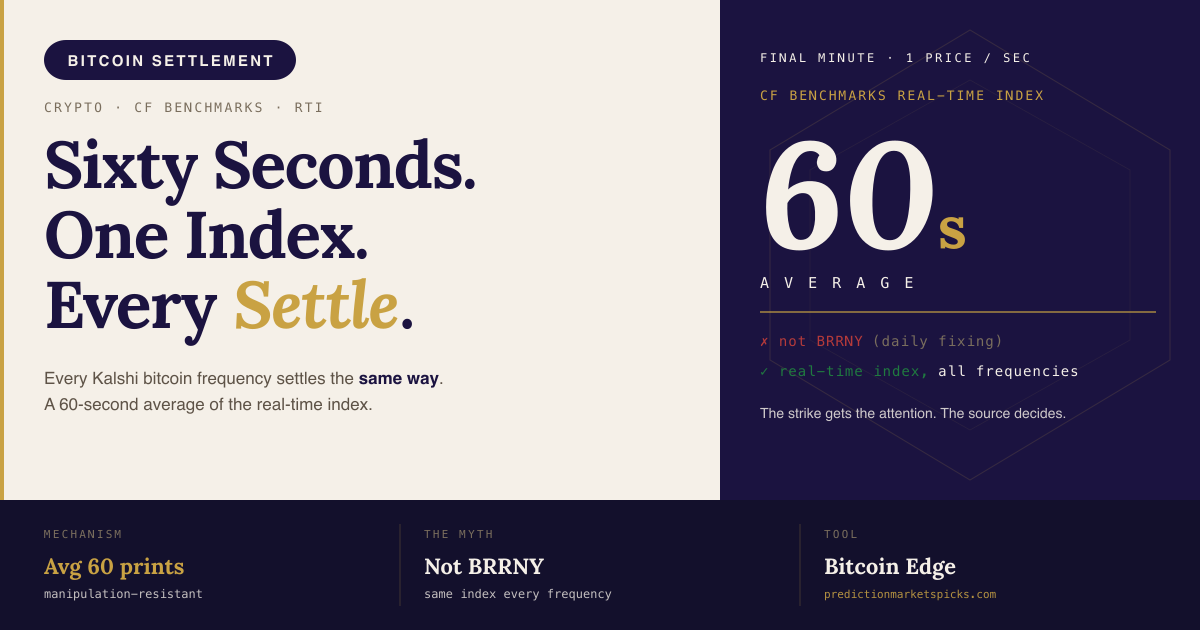

The Short Version

- One mechanism, every frequency. Kalshi settles all crypto contracts by averaging 60 seconds of the relevant CF Benchmarks Real-Time Index, sampled once per second over the final minute before the window closes.

- The bitcoin index is a continuous, multi-exchange real-time rate — not a single-venue ticker and not a once-daily fixing.

- It is not BRRNY. BRRNY is a daily fixing used for products like CME futures. Kalshi's bitcoin contracts use the real-time index, averaged over the last minute. The "BRRNY for short-dated markets" story is a myth.

- Match your spot feed to the index or your model is answering a slightly different question than the one Kalshi resolves.

The Mechanism, Exactly

Kalshi's documentation states it plainly: all crypto market contracts are settled by averaging 60 seconds of CF Benchmarks Real-Time Indexes (RTIs), which report a price once per second. Walk it through for a single contract:

1. The window has a close time — the top of the quarter-hour for KXBTC15M, the top of the hour for KXBTCD, Friday for a weekly, and so on.

2. In the final 60 seconds before that close, the relevant CF Benchmarks Real-Time Index is sampled once per second — about 60 prints.

3. Those ~60 prints are averaged into a single settlement value.

4. That average is compared to the strike. Above? The "above" / "up" side pays $1. Below? It pays $0. (And vice-versa for the opposite side.)

The CF Benchmarks Real-Time Index itself is a once-per-second benchmark that aggregates order data from the major bitcoin-USD exchanges — the same institutional reference family that underpins regulated bitcoin futures and options. It is not a single exchange's last trade, and it is not a daily fixing.

Why Average a Minute Instead of Snapping the Last Price

A last-price settlement is trivially gameable: push one large trade through a thin venue in the final second and you can nudge a contract over the line. Averaging sixty seconds of a multi-exchange index defeats that. To move the settlement, you'd have to move the index — across multiple exchanges — for a sustained minute, against everyone else's flow. That's expensive and self-defeating.

For you as a trader, the practical consequence is that the last tick you see before settlement is not the settlement price. A spike in the final ten seconds barely moves a sixty-second average. If you're holding into the close, you're holding to the average of the last minute, not to wherever the screen happens to flash at :59. Plan exits accordingly.

The BRTI vs BRRNY Myth

This is the confusion worth clearing, because two widely-cited guides get it wrong and it has metastasized into "common knowledge."

The story you'll see: short-dated bitcoin contracts (like the 15-minute) settle on one CF Benchmarks product — often miscalled "BRRNY" — while longer-dated contracts use another. It isn't true.

- The Real-Time Index is a continuous, once-per-second benchmark. This is the family Kalshi averages for settlement, at every bitcoin frequency.

- BRRNY (and its London-fixing sibling) is a once-daily fixing — a single value struck at a set time each day, designed for end-of-day NAV and futures settlement on venues like CME. It is not what Kalshi averages over the final minute of a 15-minute or hourly contract.

So when a guide tells you the 15-minute market "settles on BRRNY," it's conflating a daily fixing with a real-time index. The correct statement is the boring one: all of Kalshi's bitcoin frequencies settle on a 60-second average of the real-time index. Being right about this is exactly the kind of factual precision that earns trust — and citations — where the rest of the field is fuzzy.

Edge Cases That Cost Traders Money

The mechanism is simple. The places it bites are not:

- Your spot feed isn't the index.

- If your model prices the contract off a single-exchange ticker (a TradingView widget, one venue's API), you're modeling a price that can drift basis points — sometimes more during stress — from the averaged multi-exchange index Kalshi settles on. On a contract decided by a few dollars, that gap can erase your edge. Use a feed that aggregates the same major venues. We anchor to an aggregated real-time spot source for exactly this reason.

- The "I was right at the close" trap.

- You watched bitcoin tick above the strike at :59 and the contract still settled NO. Why? The settlement is the average of the prior 60 seconds, and the price spent most of that minute below the strike. The last tick is the loudest but the least important.

- Thin-window volatility.

- During a fast move, the 60-second average can sit well away from both the window's open and its last print. Short-dated contracts (15-minute especially) are most exposed — the averaging window is a meaningful fraction of the contract's whole life.

- Assuming the source by frequency.

- Don't infer the settlement source from the contract's duration. They're all the real-time index. The duration changes when the minute is averaged, not what is averaged.

Why This Is the Foundation of Every Edge

Settlement source is the ground truth a mispricing is measured against. Our Bitcoin Edge tool compares an options-implied probability of "bitcoin above $X" to Kalshi's own contract price for that strike. That comparison is only honest if both sides reference the same underlying price — the averaged real-time index Kalshi will actually settle on, mirrored by an aggregated spot feed on our side. Get the reference rate wrong and every edge number downstream is wrong too.

It's also why our coverage maps to where a clean second opinion exists rather than to the keyword map. The hourly rung has a live options chain to price against; the 15-minute rung does not. The settlement source is identical across both — the pricing channel available to second-guess it is not. The full frequency taxonomy lays out which rung is worth which model.

FAQ

What does Kalshi use to settle its bitcoin markets?

A 60-second average of the CF Benchmarks Bitcoin Real-Time Index, sampled once per second over the final minute before the contract window closes. The same index family is used at every frequency — 15-minute, hourly, daily, weekly, monthly, and yearly.

Does Kalshi settle bitcoin on BRRNY?

No. BRRNY is a once-daily fixing used for products like CME futures. Kalshi's bitcoin contracts settle on the continuous CF Benchmarks Real-Time Index, averaged over the last 60 seconds of each window. The "BRRNY for short-dated contracts" claim some guides make is incorrect.

Why does Kalshi average 60 seconds instead of taking the last price?

Averaging a full minute of the once-per-second index makes settlement resistant to a single-tick spike or a momentary exchange outlier. A manipulator would have to move a multi-exchange index for a sustained minute, not just print one bad trade.

Does the bitcoin settlement source change by frequency?

No. A 15-minute contract and a yearly contract settle on the same real-time index. Only the moment of the 60-second averaging window changes.

Why does the reference rate matter more than the strike?

Because the reference rate defines what "the price" means at settlement. If you model a contract against a single-exchange ticker that differs from the averaged multi-exchange index, you're pricing a slightly different question than the one Kalshi resolves — and that gap can swamp your edge.

Use The Tool

Bitcoin Edge prices the hourly KXBTCD rung against an independent options chain, anchored to the same aggregated real-time index Kalshi settles on. That alignment is the whole point — a mispricing only means something if both sides are measured against the same truth.

The strike gets the attention. The settlement source decides the outcome. Know both before you take a position.

Trade responsibly. Position size based on your edge and your account, not on excitement. Prediction-market contracts on Kalshi are regulated by the CFTC.