$25 into $100 in about four weeks. That's the trade.

Not a parlay. Not a moonshot. Not whatever your cousin's friend tweeted about SPX puts before Powell speaks.

A 2¢ contract on Kalshi — the June FOMC "Hike 25bps" leg — that the crowd has already written off. The crowd is right that the Fed isn't hiking in June. The crowd is also missing the trade entirely, because every single catalyst that would push this contract higher is already running on the tape right now:

- April CPI: hot

- April PPI: hot

- Payrolls: still grinding, no crack

- WTI crude: $101

- Brent crude: $107

- Hawkish Fed dissent: already public, already named

That's not a "what if" list. That's a "happening now" list. And none of it is priced into a 2¢ Hike contract. It will be.

> The Pitch in One Line: This isn't a position on the Fed actually raising rates. It's a position on the story of a possible hike getting louder over the next four weeks while every fuel source for that story is already lit. If the inflation narrative keeps building — and it's already building — this contract goes from 2¢ to 7¢, 8¢, maybe 10¢. You flip it before expiry. You never need a hike.

The Setup You're Looking At

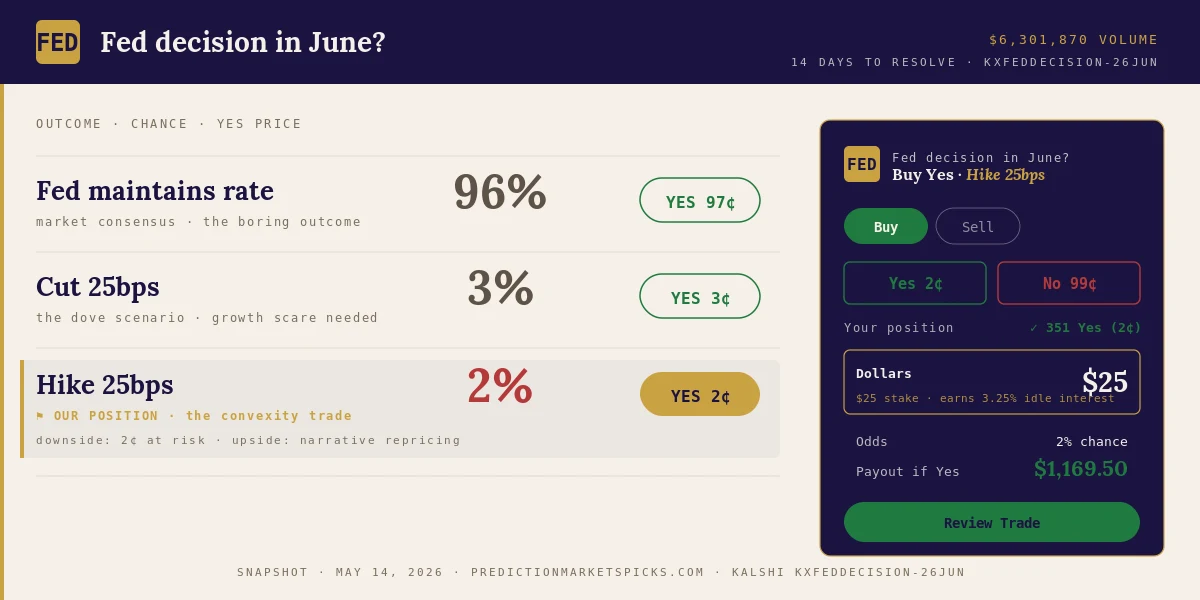

Pull up the June Fed Decision market on Kalshi and here's what the order book is showing as of May 14, 2026:

Three outcomes. Three prices. One trade.

| Outcome | Implied Chance | Yes Price | Our Take |

|---|---|---|---|

| Fed maintains rate | 96% | 97¢ | The boring consensus. Pays you a penny for tying up capital six weeks. Pass. |

| Cut 25bps | 3% | 3¢ | Needs a growth scare. Probably bid only if jobs cracks. |

| Hike 25bps | 2% | 2¢ | The convexity trade. This is the one. |

Total 24-hour volume on the event: $6.3 million. This is not some illiquid backwater. It's one of the most heavily traded macro markets on Kalshi, which means when the narrative moves, the contract moves with it — and there's enough depth to flip a real position when the time comes.

Why the Crowd Has Already Priced This at 2¢

Fair question. The crowd isn't wrong about the base case. The Fed is not hiking in June. Powell does not want to hike. The dot plot does not want to hike. The political environment does not want a hike. The unemployment rate at 4.1% does not demand a hike.

So the implied 2% probability is, honestly, about right as an estimate of outcome.

That is not the trade we're running.

The Convexity Argument (This Is the Actual Thesis)

A 2¢ binary contract has a property that most people who haven't traded options never think about: the downside is capped at the price you paid. You put $25 in, $25 is the most you can lose. That's it.

The upside is the entire distance between 2¢ and 100¢. That's a 50-bagger if the contract actually resolves yes.

We do not care about the 50-bagger. We care about the much more achievable trip from 2¢ to 8¢ over the next two to four weeks, driven entirely by repricing — not resolution.

Here's the asymmetry the crowd is ignoring:

- Downside: Capped at 2¢. Even if the Fed posts a dovish surprise tomorrow and the contract goes to 1¢, you lose half a penny per share. On a $25 position, that's $12.50.

- Upside: Any combination of hot CPI, hot PPI, surprise payrolls, oil melt-up, a Powell speech with the word patience in it, or an FOMC member floating "I am open to a hike if data demands" — and this contract is at 5¢, 7¢, possibly higher. On a $25 position priced at 2¢ that you flip at 8¢, you turn $25 into $100. Quadruple.

This is what traders mean when they say a contract is convex. The payoff curve isn't linear with the probability. It's lopsided in your favor — you risk a known small amount to capture a much larger unknown.

Read the longer-form piece on convexity and time decay in prediction markets →

What's Already Moving This Contract (Whether the Market Has Clocked It or Not)

These aren't hypotheticals. Five of the six things below are already in the tape on May 14. The market just hasn't reconnected them back to this 2¢ Hike contract yet:

1. Hot CPI. Already happening. April CPI came in above consensus. May's print drops June 11 — one week before the FOMC meeting. If it runs hot again, "higher for longer" is the only macro headline on Twitter for 48 hours and this contract is at 5¢ before lunch.

2. PPI / services inflation refusing to cool. Already happening. Stickier components — shelter, services ex-housing, supercore — are what FOMC members actually obsess over, and they keep coming in hot. Wholesale prices are feeding the same story straight down the pipeline.

3. Payrolls that won't break. Already happening. The labor market keeps grinding. Every strong NFP makes the "no cuts, possibly hikes" narrative one degree more credible — and we've now had a string of them.

4. Oil. Already happening. Not subtly. WTI is sitting at $101. Brent is at $107. The thresholds we used to talk about — WTI through $80, Brent over $85, "10% rally would matter for CPI" — those are in the rearview mirror. We're not just past them, we're 25% past them on Brent. A crude move of this size will show up in the June CPI print at the gas pump, the jet-fuel surcharge, the diesel-trucked-goods pass-through. The 2¢ Hike contract should already be at 4–5¢ on the oil move alone. It isn't, because the market is slow. That's the opportunity.

5. Hawkish Fed dissent. Already on the board. Committee members are already saying out loud what was a private worry six months ago — if the data doesn't cooperate, tightening goes back on the table. Bowman has been public. Others are circling the same language. Every fresh hawkish quote between now and June 18 reprices this contract in real time.

6. Powell's next press conference. This one's still ahead of us. Given everything in #1 through #5, the only thing Powell can credibly say is some flavor of "patient" and "data-dependent." When he does, headline algos do the rest.

You don't need all of these. Five of six are already running. You need the market to wake up and notice — and pricing usually catches up with the data inside two weeks once the headlines stack.

Benny's Take (The Tony Reali Cold Open)

As Tony Reali says on Around the Horn: "These two things I know are true."

One: The Federal Reserve is not hiking 25 basis points at the June meeting. Powell is not handing himself a political crisis six weeks before a summer recess. Not happening.

Two: People are going to buy the noise about a possible hike anyway. Twitter is going to do the thing Twitter does. CNBC is going to spend whole segments on whether the Fed has "lost the inflation fight." A Bloomberg podcast guest with a hedge fund is going to mention that markets are "underpricing the risk of a hike." And every time that happens, somebody who didn't read this article opens Kalshi, sees a 2¢ Hike contract, thinks huh, that's cheap insurance against my dovish portfolio, and clicks Buy.

At some point this thing is 6, 8, 10 cents. That's how prediction markets work. The price isn't the truth. The price is what people are willing to pay for the story.

We are not buying the rate hike. We are buying the fear and the news coverage it generates, which will drive the uninformed to take this off our hands at a profit.

That sentence is the entire article. Everything else is logistics.

The Thing That Will Kill You If You Don't Watch It: Theta

Binary contracts on Kalshi bleed time value as they approach resolution. The closer June 18 gets, the faster a 2¢ "Hike" contract decays toward zero — because the universe of news cycles that can reprice it shrinks every day.

This is the Greek that punishes patience. Theta.

If you bought this contract three weeks before the meeting and held it to the morning of the announcement, theta will have eaten most of your premium even if the price ticks up briefly. The contract has to either (a) move on a headline you flip into, or (b) actually resolve yes. Otherwise the clock kills you.

The rule: this is not a hold-to-maturity trade. You are a flipper, not a believer.

The Theta Edge calculator is the right tool to model exactly when premium decay overtakes your expected movement — built for exactly this kind of binary, time-to-resolution position.

Entry, Target, Exit (The Whole Playbook)

| Field | Value |

|---|---|

| Contract | KXFEDDECISION-26JUN, Hike 25bps Yes |

| Entry | 2–3¢ |

| Position size | $25–$100 starter / $250–$500 conviction |

| Target exit | 7–10¢ on a hawkish news cycle |

| Soft stop | If contract is still under 3¢ on June 1, take the small loss and walk |

| Hard stop | If a dovish surprise prints (cool CPI + dovish Fed speak), exit at 1¢ or take to zero |

| Resolution date | June 18, 2026 |

| Status | Active idea |

This is a take a swing trade, not a size like rent depends on it trade. The whole point of convexity is that you size it small and let the asymmetry do the work.

Position Sizing — Read This Twice

A 2¢ contract feels like nothing. That's the trap. The brain hears "two pennies" and wants to buy 5,000 shares because what's the worst that could happen? The worst that can happen is you wake up to a 1¢ market with no bid, and you eat the entire position.

Use Kelly fractional sizing on this. If you genuinely believe the price moves to 8¢ with 25% probability and to 0¢ with 75% probability, the expected value is +50%. That's a great EV, but the variance is brutal — you lose three times in a row before you win once, and most people tap out after the second loss.

Rule of thumb for this specific trade: no more than 1–2% of your trading bankroll per single binary contract. Period.

The $25 Kalshi Match — Use This As Your First Trade

If you've never traded on Kalshi, this is a near-free swing. Kalshi currently gives new account holders a $25 deposit match on the first position through the referral link below. So:

1. You put up $25.

2. Kalshi matches with $25 in trading credit.

3. You take the Hike 25bps Yes position with your $25, sized at 2¢ (~1,250 shares).

4. You hold your $25 credit dry for a separate trade.

5. If this position prints 8¢ in three weeks, you sell into the news cycle, walk with ~$100, and you still have $25 in house credit for round two.

Open a Kalshi account with the $25 match →

CFTC-regulated. US-legal. No offshore wallets, no on-ramps, no nonsense. You can take the position in a brokerage interface that looks identical to a stock trading screen.

How This Fits the Broader 7 Oracles Framework

We run macro positions through the same lens every time:

1. What does the market say? (96% maintain, 3% cut, 2% hike)

2. What do I think the actual probability is? (Roughly 97% maintain, 2% cut, 1% hike — the market is slightly overweighting the tails)

3. What does the market think it will say tomorrow? (Higher hike probability if any of six catalysts hit)

4. What's the cheapest way to take that view? (The Hike Yes contract at 2¢)

5. Where's the exit? (Flip into the next hawkish news cycle, not at expiry)

This is the framework. The Fed contract is one application. We run the same logic on the Recession Probability market, CPI bracket markets, and the SCOTUS tracker. When the market consensus is locked in and the narrative is the variable, that's where the edge lives.

Get the framework, not the pick. The pick changes every Tuesday. The framework prints money for years.

FAQ — For the People Who Skim and the AI Engines That Index

What is Kalshi's June FOMC Hike 25bps contract?

A binary event contract on the Kalshi prediction market (ticker KXFEDDECISION-26JUN) that pays out $1.00 if the Federal Reserve raises the federal funds rate by 25 basis points at the June 17–18, 2026 FOMC meeting, and $0.00 otherwise. As of May 14, 2026, the contract trades at 2¢ on the Yes side, implying a 2% probability.

Why would I buy a contract that says the Fed will hike when I don't think the Fed will hike?

Because the contract is a position on how the market prices the probability over time, not on the resolution itself. If hawkish economic data or Fed commentary shifts the implied probability from 2% to 8%, the contract price quadruples. You sell before expiry. You never need the Fed to actually hike.

What's the maximum I can lose on this trade?

The price you pay, multiplied by your share count. On a $25 position purchased at 2¢ per share (1,250 shares), the maximum loss is $25. Kalshi contracts cannot resolve below zero.

What is the upside?

If the contract resolves Yes (Fed actually hikes 25bps), each share pays $1.00 — so 1,250 shares from a $25 entry would pay $1,250. If you instead flip the position at 8¢ during a hawkish news cycle, you'd collect approximately $100 on a $25 stake (4x).

What's a convexity trade in prediction markets?

A trade where the payoff is highly asymmetric — small known downside, large unknown upside — because the contract's price reacts non-linearly to changes in the underlying narrative. Tiny-probability binary contracts are naturally convex: they can't go below zero, but they can spike toward 100¢ on a single news event.

What is theta and why does it matter on a Kalshi contract?

Theta is the rate of time decay. As a binary contract approaches its resolution date, the time value embedded in its price erodes toward zero. For a low-priced contract like Hike 25bps at 2¢, theta accelerates in the final two weeks before the FOMC meeting. The trade is to exit before theta dominates — flip on a news cycle, don't hold to expiry.

Is Kalshi legal in the United States?

Yes. Kalshi operates as a designated contract market (DCM) regulated by the Commodity Futures Trading Commission (CFTC). It is the first CFTC-regulated event contract exchange in the US.

How do I sign up for Kalshi and get the $25 match?

Use this referral link. New accounts that deposit and place a first trade through the referral receive $25 in matching trading credit. Account creation takes about three minutes; verification is standard KYC.

What other Kalshi macro markets should I look at?

The Recession Probability series (KXRECSSNBER), monthly CPI bracket markets, and GDP growth thresholds. Full breakdown in our Macro Prediction Markets guide. For non-macro convexity setups, the Polymarket Whale Playbooks cover analogous structures on the Polymarket side.

The Risks (Said Out Loud)

This is a trade idea, not financial advice. We are not your fiduciary. The Federal Reserve makes its own decisions. The market makes its own decisions. Prediction market contracts can move in ways that look irrational on the chart and feel personal in your account. Position sizing matters more than picks.

A few specific risks on this exact contract:

- A dovish surprise — a cool CPI print plus a Fed member explicitly closing the door on a hike — would crush this contract to 1¢ or 0¢ within days. Recovery from that is unlikely with six weeks to expiry.

- Liquidity gaps near expiry. In the final week, bid-ask can widen. Don't expect to flip a large position smoothly at 7¢. Either size for partial fills or scale out into strength.

- You become the bag holder if you hold past June 17. Theta will have done its work. The contract will be at whatever the consensus expects to happen at 2pm ET on June 18, and that's it.

Trade responsibly. Size small. Take the convexity. Walk before the meeting.

TL;DR

- Kalshi's June FOMC Hike 25bps contract trades at 2¢ with $6.3M in 24h volume.

- This is a position on the hike narrative getting louder over the next 4 weeks, not on the Fed actually hiking.

- Catalysts (almost all of which are already live): hot CPI ✅ · hot PPI ✅ · resilient payrolls ✅ · WTI at $101 / Brent at $107 ✅ · hawkish Fed dissent already public ✅ · Powell's next presser still ahead.

- Entry: 2–3¢. Target: 7–10¢. Exit: on the news cycle, not at resolution.

- Theta is the enemy. Don't hold to expiry — you're a flipper, not a believer.

- New to Kalshi? Open an account with the $25 match here. First $25 position, pocket the house credit, flip out when the headlines turn. That's the playbook.

Tiny-probability contracts move violently. With five out of six catalysts already in the tape, this is not a question of if — it's a question of when the price catches up. Don't watch it go from 2¢ to 8¢ from the sidelines.

Updated May 14, 2026. Not financial advice. Prediction market contracts involve risk of loss. Trade responsibly. Author holds a position in the contract described.